Best Banking-as-a-Service (BaaS) Platforms (2026)

What Is Banking-as-a-Service (BaaS)?

Banking-as-a-Service (BaaS) is the delivery of regulated banking capabilities -- accounts, cards, payments, lending, KYC, and compliance -- through APIs, so non-bank companies can embed financial services into their own products without becoming a licensed bank. A licensed bank sits in the background holding deposits and the charter; the BaaS provider handles orchestration and compliance tooling; and the customer-facing brand owns the user experience. The broader fintech-as-a-service market is valued at roughly $135.72 billion in 2026. Critically, the category has been reshaped by the 2023--2024 regulatory tightening and several high-profile BaaS failures, making compliance depth and bank-relationship structure the decisive selection criteria.

What is the best Banking-as-a-Service (BaaS) platform in 2026?

The best BaaS platform in 2026 is Treasury Prime for fintechs that want control over bank relationships -- its multi-bank model gives you direct contracts with multiple partner banks, pricing leverage, and ~2-week go-live. Unit is the most developer-friendly all-in-one option, Synctera is the most compliance-first, and Stripe Treasury is best if you're already on Stripe.

Best for your situation

- ▸Control over bank relationships: Treasury Prime -- multi-bank model

- ▸Developer-first all-in-one: Unit -- simplest API & pricing

- ▸Compliance-first: Synctera -- community banks, deep BSA tooling

- ▸Already on Stripe: Stripe Treasury -- no new infrastructure

VERIFIED PLATFORM DATA (2026)

| Platform | Model | Region | Key Detail |

|---|---|---|---|

| Treasury Prime | Multi-bank, direct contracts | US | 2M+ accounts, 15+ banks, $103M funding, ~2-wk go-live |

| Unit | All-in-one, single-vendor | US | Founded 2019, NY; developer-friendly, simpler pricing |

| Synctera | Community-bank matching | US | Founded 2020; $94M raised; compliance-first |

| Stripe Treasury | Stripe-ecosystem | US | Partners Goldman Sachs, Evolve Bank |

| Column | Chartered bank (own license) | US | Direct bank access, no BaaS middleman |

| Griffin | Fully licensed (PRA/FCA) | UK | Holds funds at Bank of England |

| Solaris / Swan | Licensed BaaS | EU | Accounts, cards, lending (Solaris); SEPA (Swan) |

Why Compliance Structure Now Decides BaaS Choice (2026)

The 2023--2024 BaaS shakeout changed the rules. Before, speed-to-launch was the selling point and seed-stage startups onboarded easily. After, regulators tightened oversight, several middleware BaaS providers failed, and banks narrowed risk appetite. Now in 2026, providers raised the bar -- many accept mainly Series C+ or public-company fintechs. Compliance, reconciliation, and BSA tooling are now core product, not afterthoughts. "Direct" bank-contract models (Treasury Prime, Column) reduce the tri-party risk that caused several high-profile collapses.

How BaaS Models Differ (and Why It Matters)

THREE BaaS STRUCTURES (2026)

| Model | Providers | How It Works | Trade-off |

|---|---|---|---|

| Multi-Bank / Direct Contract | Treasury Prime | You hold direct contracts with multiple banks; pricing leverage; swap or add banks; less lock-in | You own more of the compliance program |

| Single-Vendor / All-in-One | Unit, Synctera, Stripe Treasury | One platform orchestrates the bank relationship; simpler to start; turn-key compliance tooling | More dependence on the provider |

| Own-License / Chartered | Column (US), Griffin (UK) | The provider IS the bank -- no middleman layer; removes tri-party risk entirely | Less flexibility than multi-bank |

Featured Fintech

Treasury Prime -- Best Overall for Bank-Relationship Control

Treasury Prime is the best overall BaaS platform in 2026 for fintechs and companies that want control over their bank relationships. Unlike single-vendor models, Treasury Prime acts as the connective layer between you and multiple banks -- giving you direct contracts with several partner banks, which means pricing leverage, redundancy, and the ability to add or swap banks without rebuilding. It has powered 2M+ accounts and connects to 15+ partner banks.

TREASURY PRIME AT A GLANCE

| Attribute | Detail |

|---|---|

| Accounts opened through platform | 2 million+ |

| Partner banks in network | 15+ |

| Total funding | $103M (Series C) |

| Go-live speed | ~2 weeks (vs 4--6 weeks for some rivals) |

| Named bank partners | OceanBank, Grasshopper, and others |

| Region | US only |

| Reconciliation | Real-time (vs batch processing elsewhere) |

Honest Limitation

The flip side of control is responsibility -- with direct bank contracts, you own more of the compliance program than you would with a fully turn-key provider. Treasury Prime is US-only, so it's not an option for companies needing EU or UK banking. The enterprise model suits scaling fintechs more than very early-stage experiments.

Best For

Growth-stage US fintechs and platforms that want multiple bank relationships, pricing leverage, real-time reconciliation, and resilience against single-provider risk.

Unit -- Best Developer-First All-in-One Platform

Unit is the most developer-friendly all-in-one BaaS platform -- providing accounts, wallets, money movement, card issuing, and capital access through a clean API, with simpler pricing than Treasury Prime's enterprise model. It's purpose-built for embedding banking into vertical SaaS and business-management software.

UNIT PLATFORM OVERVIEW

| Feature | Detail |

|---|---|

| Core offering | All-in-one embedded finance: accounts, cards, payments, lending in one API |

| Developer experience | Developer-friendly with simpler, more transparent pricing |

| White-label products | White-label checking and money-movement products |

| Founded / HQ | 2019, New York |

| Best fit | Vertical SaaS adding banking features |

| Region | US |

Honest Limitation

Single-vendor model means more dependence on Unit's bank relationships than Treasury Prime's multi-bank approach. Like the rest of the category, Unit has raised its client bar post-2024, favouring more established fintechs.

Best For

Mid-sized SaaS businesses and developer-led teams adding banking capabilities to their product who value API simplicity over multi-bank flexibility.

Synctera -- Best Compliance-First Platform

Synctera is the most compliance-first BaaS platform -- it matches fintechs with the right US community bank partner and wraps the relationship in deep compliance, BSA, reconciliation, and fraud tooling. It positioned itself well for the post-2024 regulatory environment by treating compliance as a core product, not an add-on.

SYNCTERA PLATFORM OVERVIEW

| Feature | Detail |

|---|---|

| Core model | Community-bank matching with compliance-as-a-service |

| Compliance tooling | Deep BSA, reconciliation, and fraud tooling as core product |

| Banking experience | Co-branded, turn-key banking experiences |

| Notable customers | Bolt; partnership with AI financial-crime firm Hawk |

| Funding | $94M raised |

| Founded / HQ | 2020, Palo Alto |

Honest Limitation

Like Treasury Prime and Unit, Synctera now tends to accept mainly Series C+ or public-company fintechs as banks narrow risk appetite. Focused on the US market.

Best For

Fintechs that prioritise compliance robustness and want turn-key co-branded banking with strong BSA and fraud tooling built in.

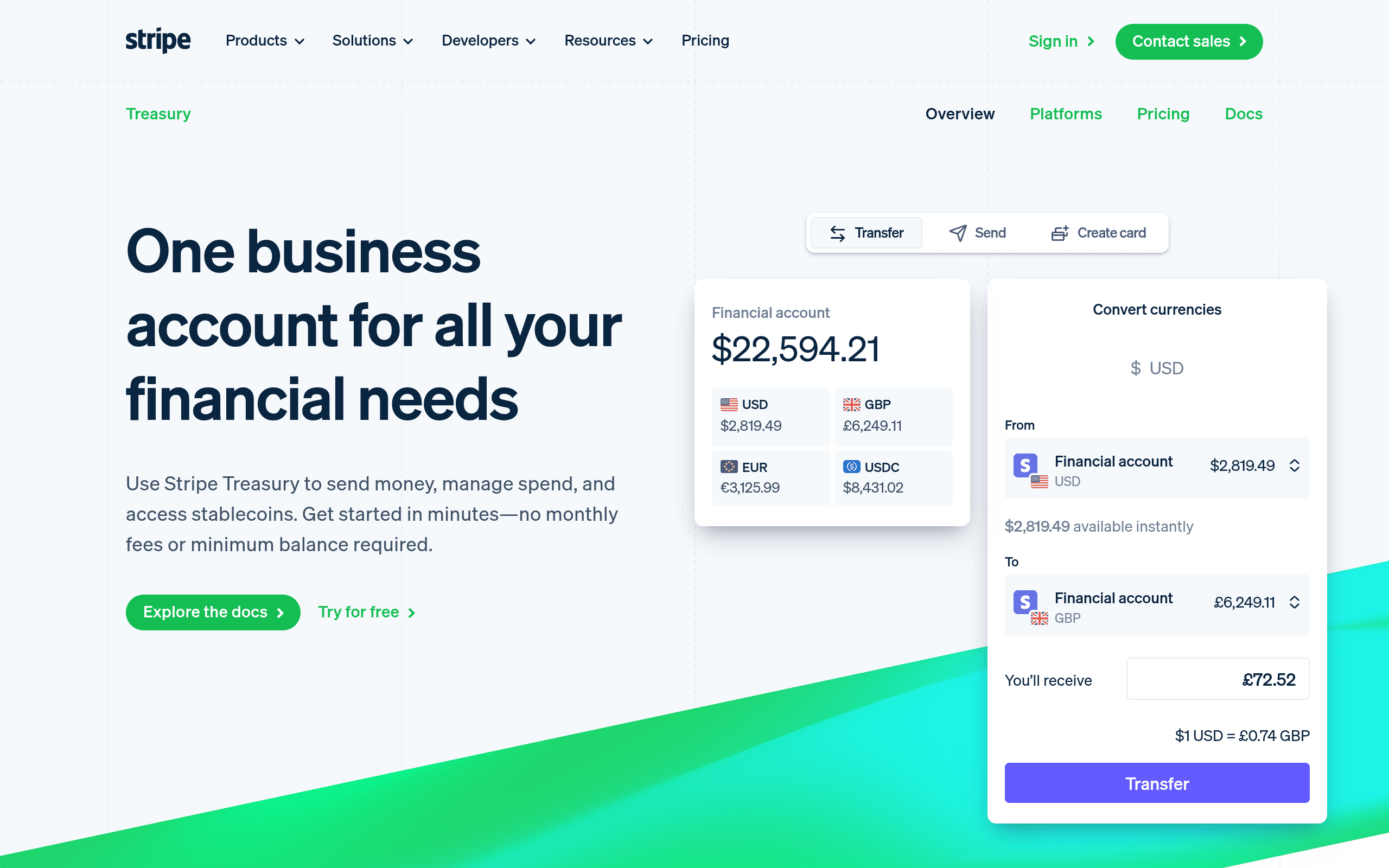

Stripe Treasury -- Best for Stripe-Ecosystem Platforms

Stripe Treasury is the most accessible BaaS option for companies already embedded in Stripe's ecosystem. It lets platforms offer FDIC-insured financial accounts, ACH transfers, wires, and card issuing directly inside their existing Stripe environment, partnering with established banks like Goldman Sachs and Evolve Bank to hold deposits.

STRIPE TREASURY PLATFORM OVERVIEW

| Feature | Detail |

|---|---|

| Core offering | Embedded banking inside the existing Stripe/Stripe Connect environment |

| Account type | FDIC-insured accounts, ACH, wires, and card issuing |

| API approach | API-first approach familiar to Stripe developers |

| Bank partners | Goldman Sachs, Evolve Bank |

| Prerequisite | Stripe Connect account required |

| Region | US |

Honest Limitation

Most valuable if you're already on Stripe; adopting it purely for BaaS means buying into the Stripe ecosystem. Transaction-based pricing requires volume modelling.

Best For

Software platforms already using Stripe Connect that want to add embedded banking without switching infrastructure providers.

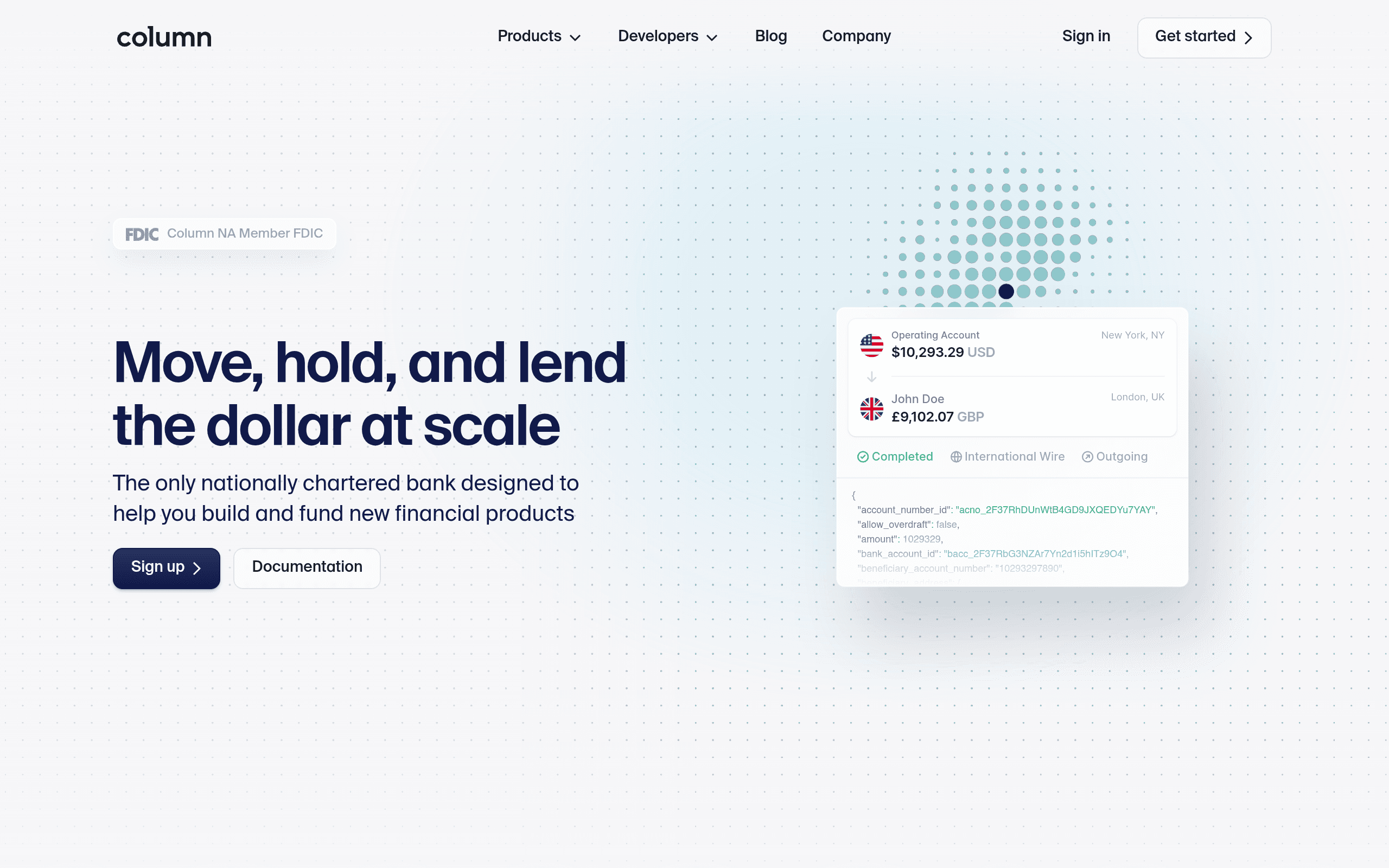

Column -- Best for Removing the Middleman

Column is a nationally chartered bank built for developers -- meaning there's no BaaS middleman between you and the bank. Its proprietary core gives direct bank access via API for accounts, payments, and lending, eliminating the tri-party structure that caused several BaaS failures.

COLUMN PLATFORM OVERVIEW

| Feature | Detail |

|---|---|

| Charter | Nationally chartered bank |

| Architecture | Developer-first API with proprietary banking core |

| Key advantage | Direct bank access -- no intermediary platform layer |

| Capabilities | Accounts, payments, and lending via API |

| Risk structure | Structurally removes tri-party risk |

| Region | US |

Honest Limitation

Less flexibility than a multi-bank model (you're on Column's charter), and the developer-first, no-hand-holding approach suits technically strong teams more than those wanting turn-key support.

Best For

Developer-strong fintechs that want direct, chartered-bank access via API and prefer to eliminate the BaaS middleman entirely.

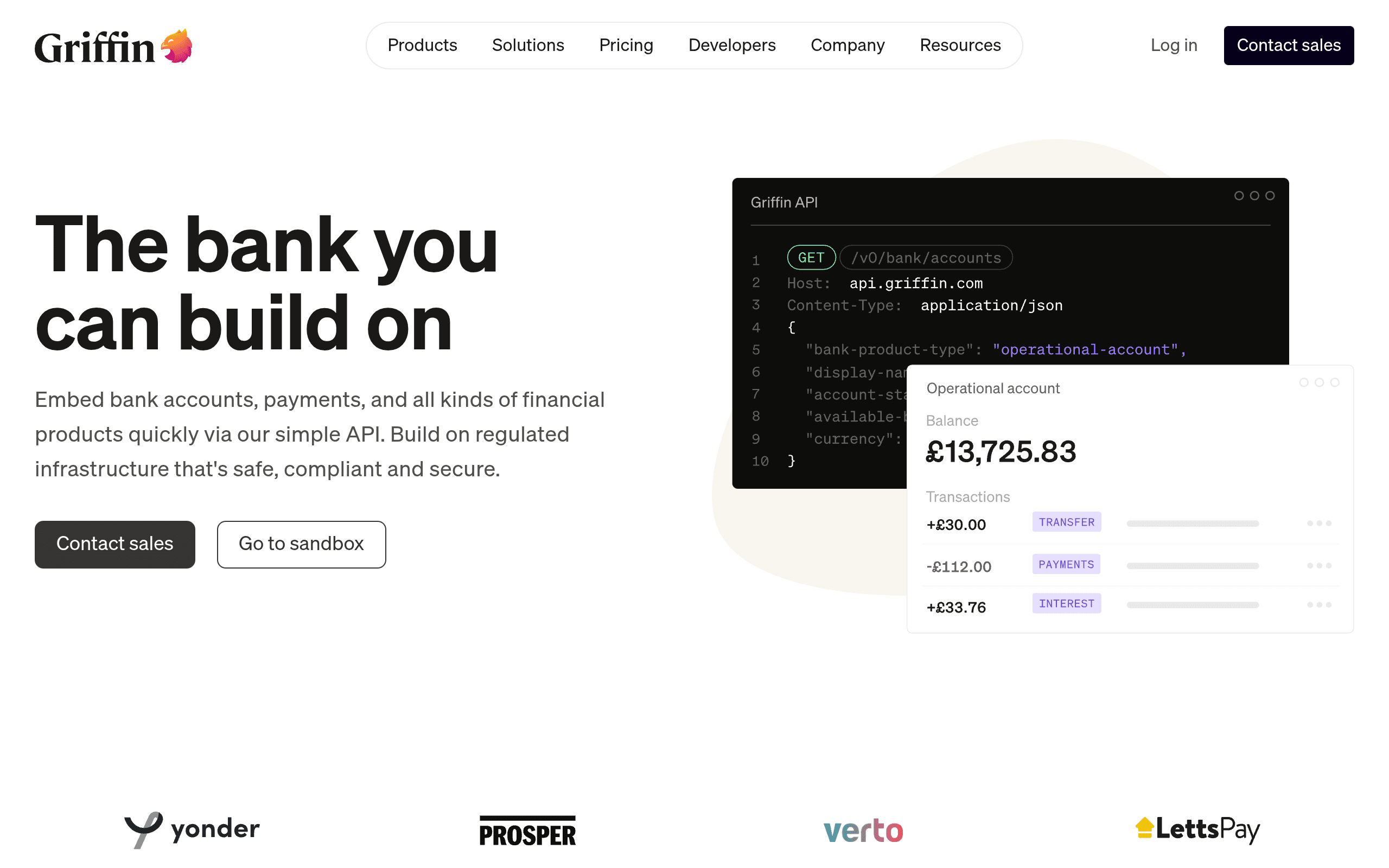

Griffin -- Best for UK-Licensed Banking

Griffin is a UK BaaS platform with a full banking license from the PRA/FCA and direct Bank of England access. It doesn't lend out customer deposits -- it holds all funds at the Bank of England, providing a high level of security and transparency for end users.

GRIFFIN PLATFORM OVERVIEW

| Feature | Detail |

|---|---|

| License | Full UK banking license (PRA/FCA) |

| Deposit security | Holds all customer funds at the Bank of England (no fractional lending) |

| API approach | API-first delivery |

| Capabilities | Accounts, payments, and compliance for UK financial services |

| Pricing | Transaction-based pricing with volume discounts |

| Region | UK |

Honest Limitation

UK-focused, so not suitable for US or broad EU needs. The fully-licensed, safety-first model trades some flexibility for security.

Best For

Regulated financial-services companies operating in the UK that want a fully-licensed provider with maximum deposit security.

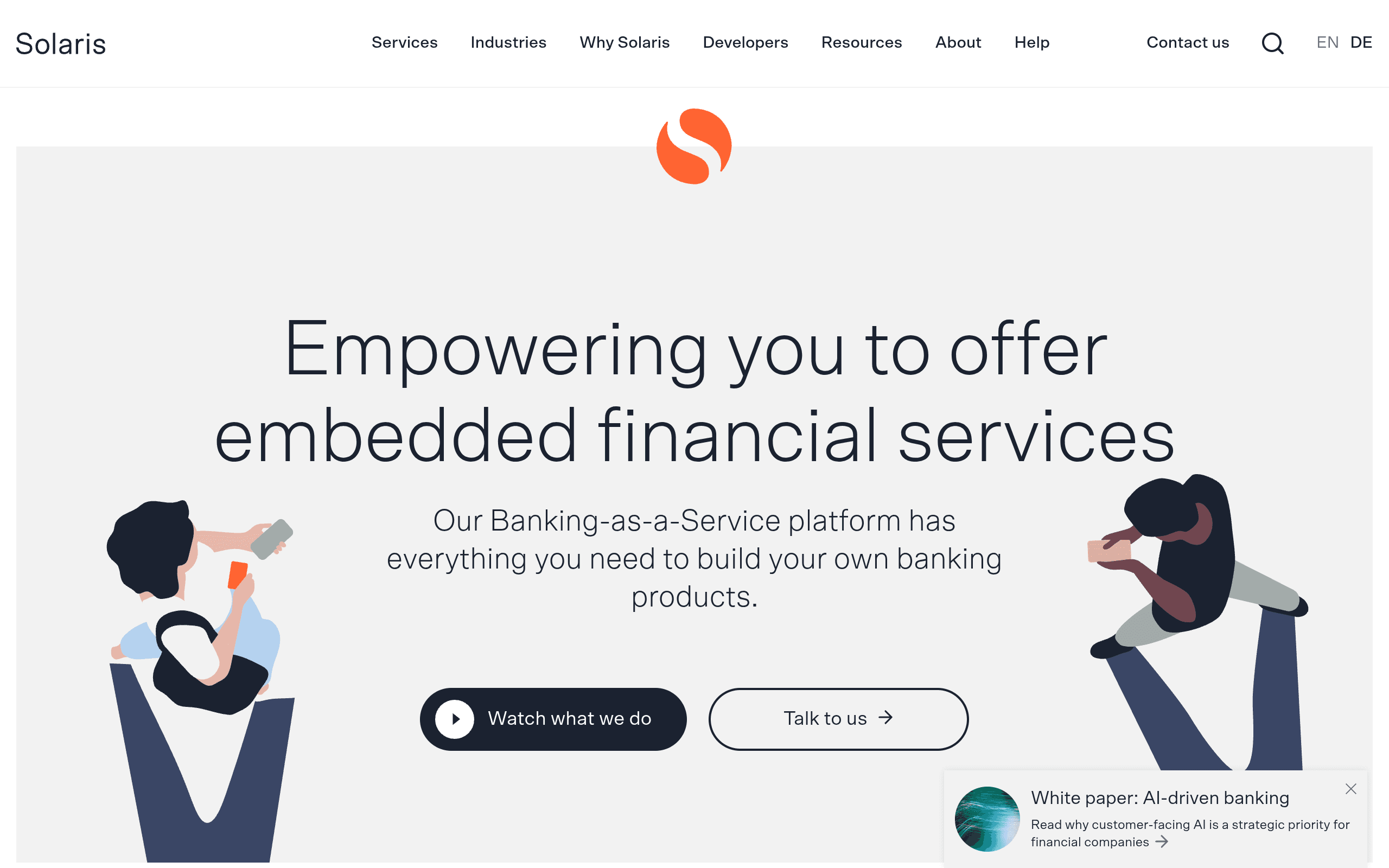

Solaris & Swan -- Best for European Coverage

For companies needing EU banking, Solaris and Swan are the leading licensed BaaS providers. Solaris holds a full European banking license and offers accounts, cards, lending, and even crypto across the EU. Swan specialises in embedded SEPA accounts and cards for European platforms.

SOLARIS & SWAN OVERVIEW

| Feature | Solaris | Swan |

|---|---|---|

| License | Full EU banking license | Licensed payment institution |

| Capabilities | Accounts, cards, lending, crypto | Embedded SEPA accounts and cards |

| Developer experience | Enterprise-grade API | Developer-friendly, modern API |

| Region | EU-wide | EU-wide (SEPA zone) |

| Compliance | Regulatory compliance for European markets | Regulatory compliance for European markets |

| Best fit | Full-stack EU banking | Embedded SEPA for platforms |

Honest Limitation

EU-focused; not the choice for US or UK banking needs. As with all licensed providers, onboarding and compliance requirements are substantial.

Best For

European fintechs and platforms embedding SEPA accounts, cards, or lending across the EU.

Frequently Asked Questions

What is the best Banking-as-a-Service (BaaS) platform in 2026?

For US fintechs wanting control and resilience: Treasury Prime -- its multi-bank model gives you direct contracts with multiple partner banks, pricing leverage, real-time reconciliation, and ~2-week go-live, with 2M+ accounts of proven scale. For developer-first simplicity: Unit. For compliance-first turn-key banking: Synctera. For Stripe users: Stripe Treasury. For the UK: Griffin. For the EU: Solaris or Swan.

What is Banking-as-a-Service (BaaS)?

BaaS is the delivery of regulated banking capabilities -- accounts, cards, payments, lending, KYC, and compliance -- through APIs, so non-bank companies can embed financial services into their own products. A licensed bank sits in the background holding deposits and the charter; the BaaS provider handles orchestration and compliance tooling; and the customer-facing brand owns the user experience. You don't become a bank -- you rent a bank's regulated capabilities.

How did the 2023-2024 BaaS failures change the market?

Several middleware BaaS providers failed and regulators sharply increased oversight, exposing the risks of the tri-party (fintech-platform-bank) model. As a result, providers raised their client bar -- many now accept mainly Series C+ or public-company fintechs -- and made compliance, reconciliation, and BSA tooling core product rather than an afterthought. "Direct" bank-contract models (Treasury Prime, Column) gained favour because they reduce the intermediary risk that caused several collapses.

In 2026, compliance structure is the first thing to evaluate.

What's the difference between a multi-bank and single-vendor BaaS model?

A multi-bank model (Treasury Prime) gives you direct contracts with several partner banks, providing pricing leverage, redundancy, and the ability to add or swap banks -- but you own more of the compliance program. A single-vendor model (Unit, Synctera, Stripe Treasury) routes everything through one platform's bank relationship, which is simpler to start and offers turn-key compliance tooling, but creates more dependence on that single provider.

Do I need a banking license to use a BaaS platform?

No -- that's the entire point of BaaS. The provider partners with a licensed bank that holds the charter, FDIC insurance (in the US), and regulatory responsibility, while you integrate via API. However, you'll still need your own KYC/AML processes, and depending on your activities you may need state money-transmitter licenses for certain payment functions. The provider handles the bank charter; you remain responsible for your program's compliant operation.

About Geeky Expert

Geeky Expert is a leading provider of research and insights, dedicated to helping businesses make informed decisions through comprehensive analysis.